- Home

- About us

- News

- Events

- EXPORT Export

-

BUY

Buy

BuyBuyFood and beverage Beef Caviar Dairy Products Fruits Healthy foods Olive oil Processed Foods Rice Sweets, honey and jams Wines ICT Software development Technology products

- INVEST Invest

- COUNTRY BRAND Country Brand

-

INFORMATION CENTER

Information center

InformationCenterInformationCenterReports Country reports Department reports Foreign trade reports Product-Destination worksheet Sectors reports Work documentsStatistical information Classification Uruguay XXI Exports Imports Innovative National Effort Macroeconomic Monitor Tools Buyers Exporters Investors

- Contact

-

Languages

slide

1 of 1

Tax System

Tax System

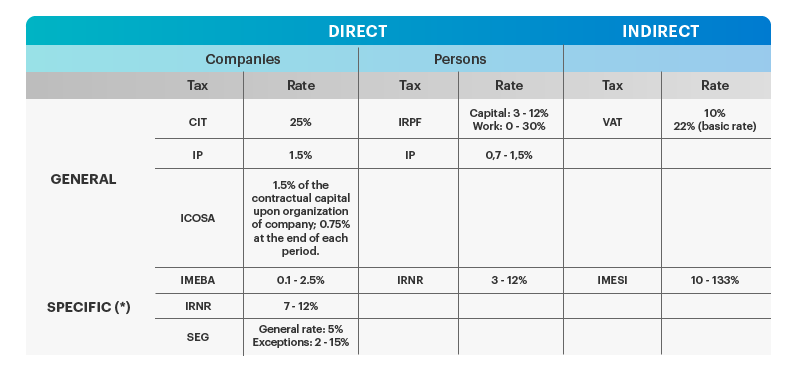

The Uruguayan tax system includes both indirect and direct taxes which apply the source principle.

Main taxes in Uruguay related to the specific business activity

(*) Although all cases require a triggering event, specific taxes that have a limited scope as they apply to specific products or sectors or specific types of companies or individuals.

Direct taxes applied in Uruguay to companies include mainly the Corporate Income Tax (IRAE) at a rate of 25% and the Net Worth Tax (IP) at a rate of 1.5%. Only income from Uruguayan source is levied, and no tax credit is granted for taxes levied abroad, unless there are double taxation agreements in force.

The main direct tax levied on individuals is the Personal Income Tax (IRPF). It is personal, direct, and progressive and levied on income obtained by individuals residing in Uruguay.

Income of Uruguayan sources obtained by non-resident natural or legal persons without permanent establishment in the country is subject to the Non-Resident Income Tax (IRNR). IRNR is applied at proportional rates ranging from 3% to 12%, depending on the type of income.

The main indirect taxes include the Value Added Tax (VAT) and Excise Tax (IMESI). The basic rate is 22%, with a minimum rate of 10% only applicable to certain products and services. Exports and circulation of most agricultural products are applied the zero rate regime, whereby tax credit is reimbursed.

The Excise Tax (IMESI) is applied to the first disposal at any title carried out by producers or importers of certain products, excluding exports. Main products which fall under this category are fuel, tobacco, beverages, cosmetics and cars and the rate varies according to the item.

At the time of assessing any investment in Uruguay, be aware that the country has a wide range of incentives which, among other benefits, allows investors to discount the investment made from future income levied by IRAE. For more information, refer to the Investment Promotional Schemes chapter.